Podcast: Play in new window | Download

Reading Time: 3 minutes

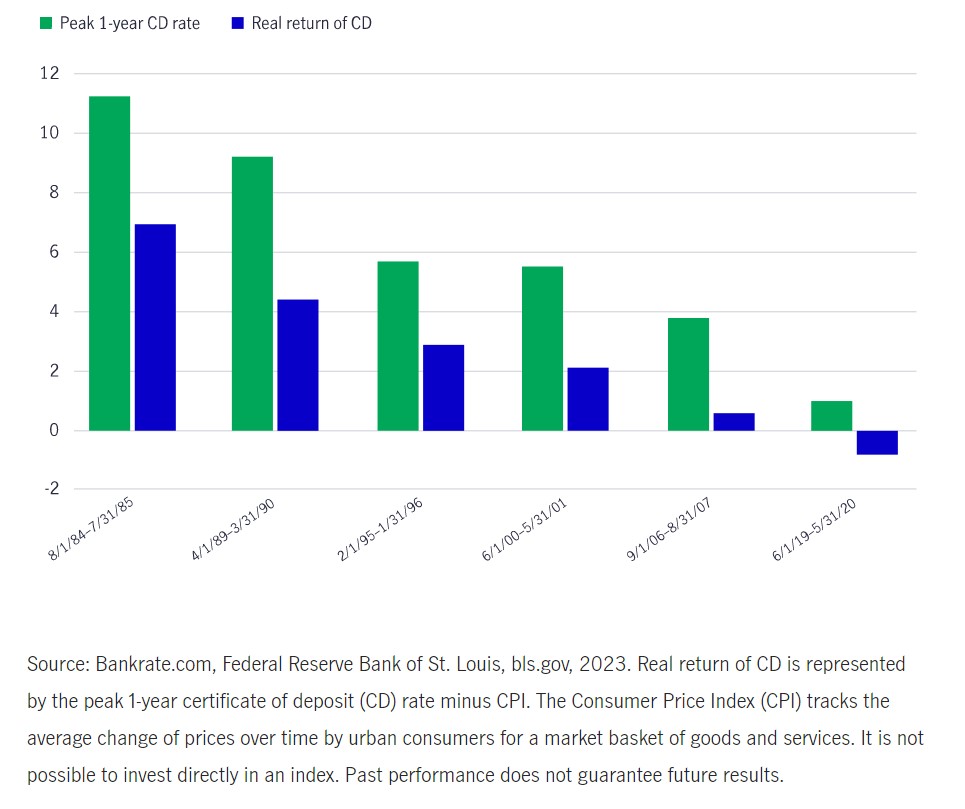

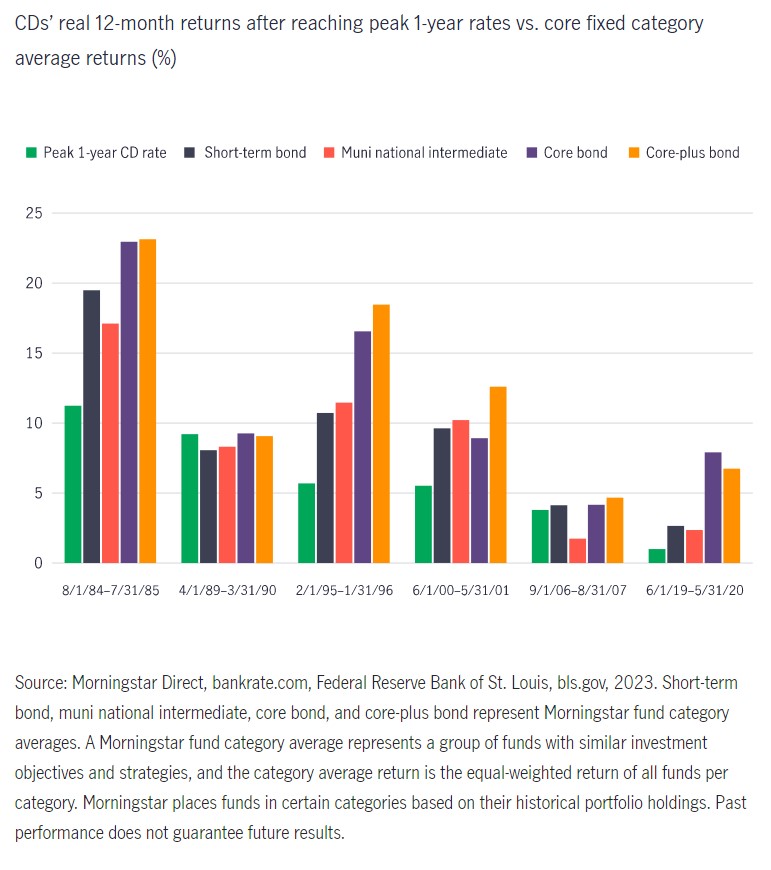

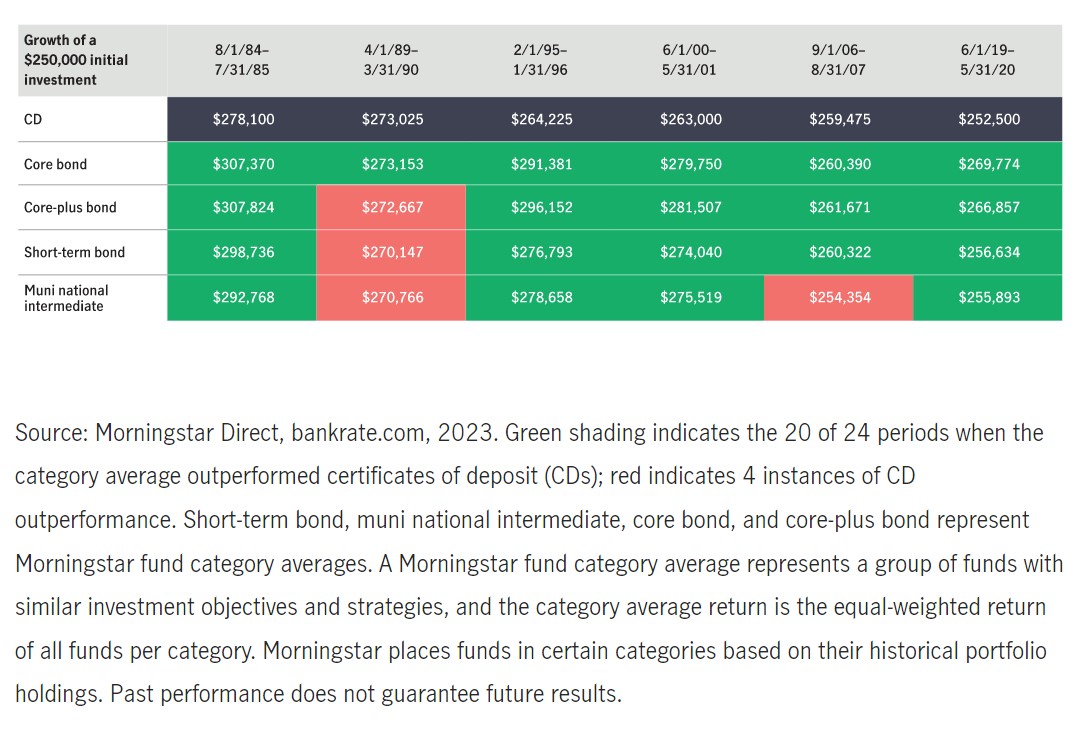

In a recent episode of Intelligent Money Minute, we had the pleasure of interviewing Larry Swedroe, the head of Financial and Economic Research at Buckingham Strategic Wealth. Our discussion centered around the dangers of recency bias, a common emotional tendency among investors. Larry emphasized the importance of understanding historical context and avoiding the trap of projecting recent events onto the future. In this blog post, we’ll share some key takeaways from our conversation and explore strategies to overcome recency bias in investment decision-making.

Reading Time: 3 minutes

In a recent episode of Intelligent Money Minute, we had the pleasure of interviewing Larry Swedroe, the head of Financial and Economic Research at Buckingham Strategic Wealth. Our discussion centered around the dangers of recency bias, a common emotional tendency among investors. Larry emphasized the importance of understanding historical context and avoiding the trap of projecting recent events onto the future. In this blog post, we’ll share some key takeaways from our conversation and explore strategies to overcome recency bias in investment decision-making.