Reading Time: 5 minutes

The winter chill has settled in once again, and with it comes memories of last year’s ice-skating adventure—the one that left me with a humbling lesson in balance, vulnerability, and, ultimately, a torn rotator cuff. Read more here. Since then, physical therapy, an MRI, and a well-placed steroid shot have been part of my journey back to health. This winter, though the shoulder pain persists, I find myself reflecting not on my stumble, but on a different kind of ice experience: hockey. Specifically, the wisdom of The Great One, Wayne Gretzky.

Gretzky famously said, “I skate to where the puck is going to be, not where it has been.” This insight into anticipating the game’s flow offers a perfect parallel to Intelligent Investing’s approach to wealth management. Just as Gretzky knew that success lay in anticipating the puck’s path, successful investing often requires a similar foresight—positioning yourself not based on where the markets are today, but where they are likely heading.

Resilience on Ice and in Markets

My recovery from the torn rotator cuff hasn’t been linear. There were setbacks, discomfort, and the need for physical therapy. But through resilience and the guidance of professionals, progress was made. Investing is much the same. Markets will fall. Asset classes will go out of favor. But patience, discipline, and a strategic approach—skating to where the puck is going—help us navigate volatility and emerge stronger.

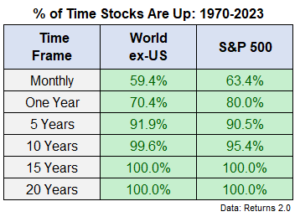

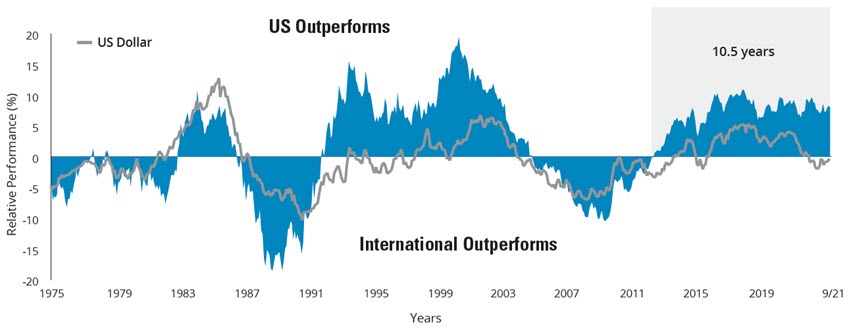

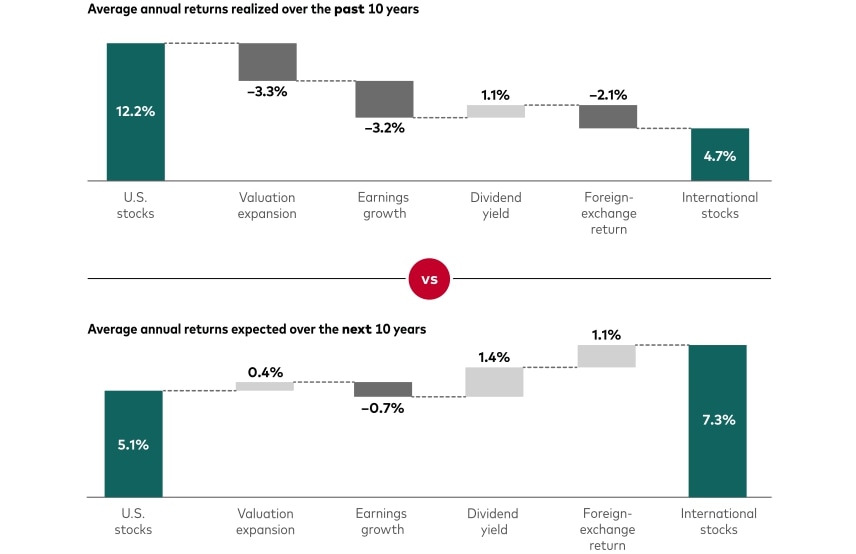

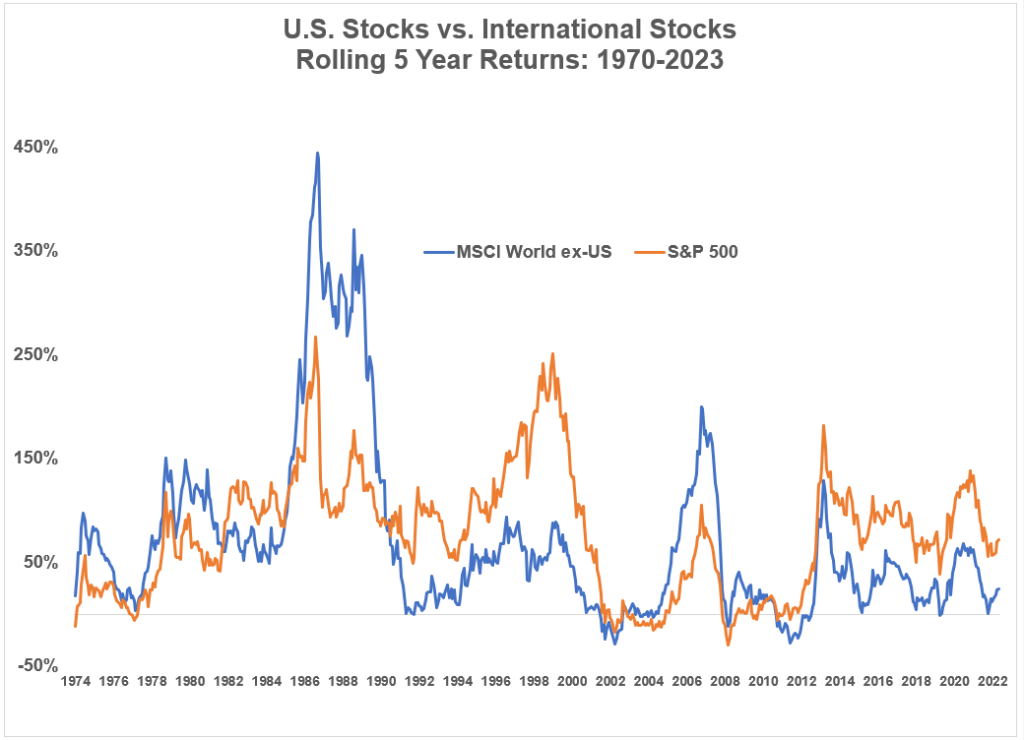

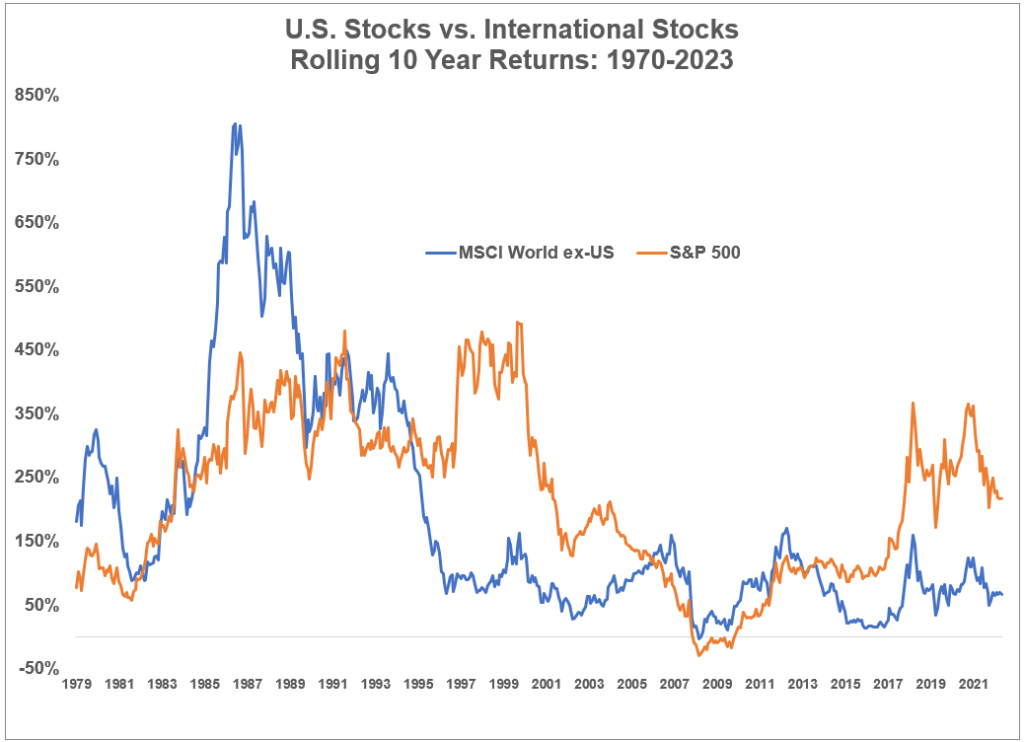

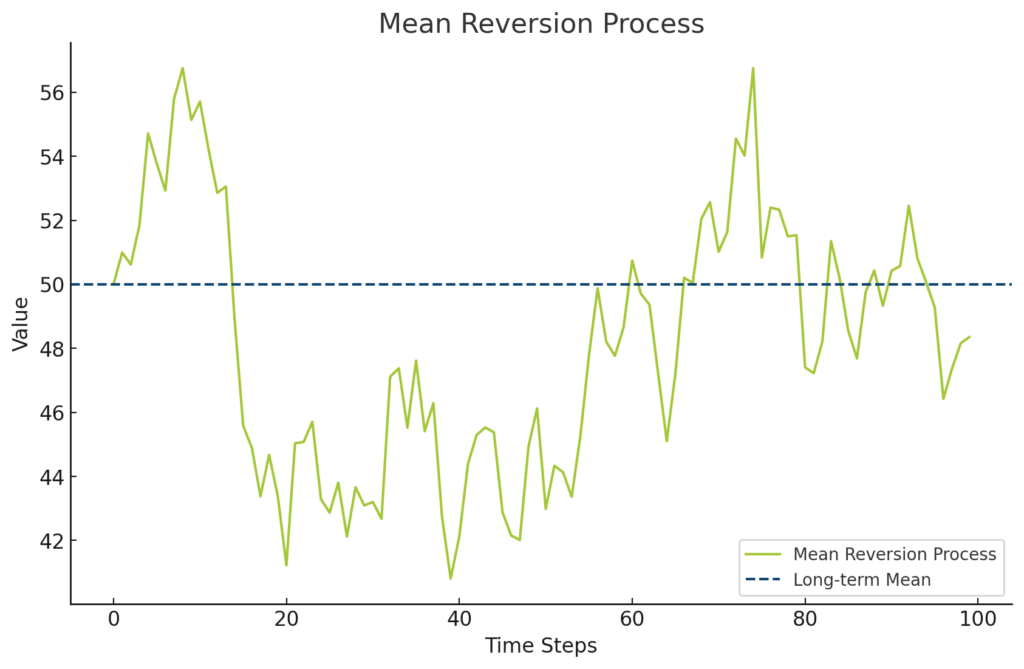

Just like a skilled hockey player anticipates where the puck is going, not where it has been, investing wisely involves understanding where markets may be heading based on historical trends and valuation metrics. Markets exhibit a strong tendency toward mean reversion—when an asset class moves significantly above or below its historical average, it often eventually returns to that average. For instance, periods of extreme market exuberance or pessimism rarely last forever.

High valuations may correct downward, while undervalued assets often rebound. Disciplined rebalancing helps capitalize on this principle by strategically reallocating investments when certain assets deviate too far from their mean. This disciplined approach avoids chasing inflated markets and positions investors to benefit when temporarily depressed assets eventually revert back toward their historical norms.

Intelligent Investing’s Game Plan

At Intelligent Investing, we act as fiduciaries, committed to helping our clients make decisions that are in their best interest. Our proprietary Intelligrations® software we developed in-house integrates various financial technologies to create a clearer picture of your financial situation. We organize financial complexities, identify opportunities, and develop strategies that anticipate market movements rather than chase past performance.

- Minimizing Fees – Including taxes and unnecessary costs.

- Family Focus – Ensuring financial communication aligns across generations.

- Maximizing Time – So you can focus on what matters most.

- Leveraging Technology – To improve decision-making and behavior.

The Market’s Icy Terrain

Much like the ice rink I skated on last year, markets can be unpredictable, slippery, and occasionally rougher than anticipated. Many investors find themselves chasing recent performance, drawn to what has been successful. A prime example is Bitcoin and other cryptocurrencies. Over the past year, Bitcoin has surged, driven by a combination of factors—growing institutional acceptance, macroeconomic trends, and notable endorsements. The recent shift by figures like President Trump and Elon Musk toward favoring cryptocurrency has thrown speculation into full throttle, fueling a renewed frenzy.

While it’s tempting to jump in, history reminds us that chasing past success can lead to regret. The dot-com bubble of the early 2000s and the real estate crash of 2008 are cautionary tales of euphoria-driven investments that ultimately crumbled. I’m not suggesting that cryptocurrencies or Bitcoin are destined for the same fate, but prudence advises against investing out of a fear of missing out (FOMO). Emotional decisions driven by hype and speculation often lead to financial missteps.

The Antidote: Disciplined Rebalancing

Instead of reacting to the latest market headlines, a disciplined rebalancing approach offers a structured way to maintain investment integrity. At Intelligent Investing, we emphasize rebalancing portfolios based on each client’s risk tolerance and their Investment Policy Statement (IPS). This disciplined process ensures that portfolios stay aligned with long-term goals rather than being swayed by short-term market excitement.

When certain asset classes outperform and others lag behind, portfolios naturally drift from their target allocations. Rebalancing involves selling portions of the investments that have grown beyond their intended allocation and buying more of the assets that have temporarily declined. This approach effectively forces investors to do what many find difficult—selling high and buying low.

Rebalancing in Action

Imagine a scenario where equities have a strong year, increasing their share in a balanced portfolio. While it’s tempting to let those gains ride, disciplined rebalancing prompts us to take profits by selling some of those equities and reallocating to underperforming assets like bonds or other sectors that may be temporarily down. This method reduces the risk of becoming overexposed to a single asset class and helps maintain a portfolio that aligns with your risk profile and financial goals.

Avoiding Emotional Pitfalls

Rebalancing isn’t just a mechanical process; it’s a powerful way to manage investor behavior. When markets are soaring, it helps temper greed. When markets are falling, it can mitigate fear. Instead of chasing the latest “hot” investment, rebalancing keeps you grounded in a strategy designed to weather market volatility. It provides a framework that helps avoid emotional pitfalls, such as the fear of missing out or panic-driven decisions.

Ready to Skate Ahead?

As we step further into 2024, let’s remember that investing, like ice hockey, is a game of anticipation, discipline, and resilience. If you’re ready to skate toward where the financial puck is going, not where it’s been, we’d love to partner with you. Whether through a call or a coffee, let’s discuss how Intelligent Investing can help guide you toward financial success.

At Intelligent Investing, our disciplined approach to rebalancing, guided by our clients’ Investment Policy Statements, aims to keep portfolios aligned with individual goals and risk tolerances. Our proprietary Intelligrations® technology helps us efficiently manage and monitor portfolios, ensuring they stay balanced in a way that reflects our clients’ needs, not the latest headlines.

As we finish 2024, remember that maintaining discipline—whether on the ice or in the markets—is key to long-term success. Chasing the latest investment trend may feel exciting, but a well-balanced portfolio tailored to your goals is what truly paves the way for financial resilience and growth.

If you’d like to explore how a disciplined rebalancing strategy can help you stay on course, we’d love to connect—whether over a call or a coffee. At Intelligent Investing, we’re here to help you navigate the icy terrain of the markets with confidence and clarity.

P.S. – For more on embracing vulnerability and financial transparency, check out my previous blog post, Getting Naked. It might just change how you think about your financial journey

Schedule a short discovery call or meeting