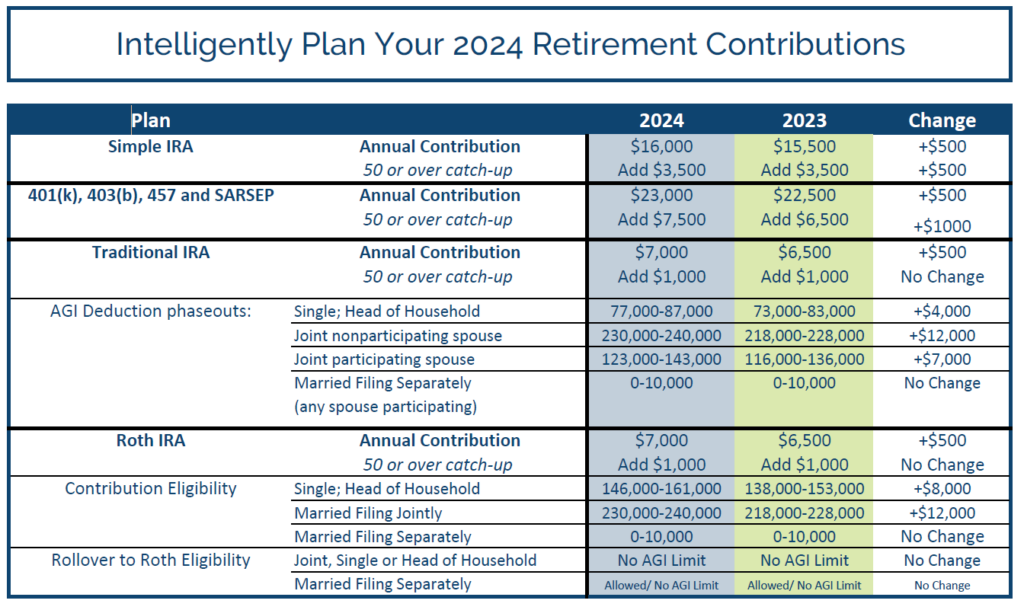

We all know it is important to plan for the future. This is a time of year where we set new resolutions and a great time to make a plan for your investable dollars. Note the following chart which shows the annual savings limits of the plan for this year and adjust your savings to take full advantage of the annual contributions. Remember, a missed year is a missed opportunity that does not come back.

We love automating this for our clients to improve their behavior and increase their odds of reaching their goals.

How to Use the Above Chart

Identify the type(s) of retirement saving that you currently use.

If you are 50 years or older, add the catch-up amount to your potential savings total.

Take note of the income limits within each plan type. For traditional IRA’s, if your income is below the noted threshold, your taxable income is reduced by your contributions. The deductibility of your contributions is also limited if your spouse has access to a plan. In the case of Roth IRAs, the income limits restrict who can participate in the plan.

Consider setting up new accounts for a spouse and set up automatic savings on a regularly-scheduled basis.

Please click here to connect with us if you need help in automating your contributions to help you reach your long-term retirement goals.