Reading Time: 4 minutes

A Time-Tested Strategy Under Scrutiny

The 60/40 portfolio, composed of 60% U.S. stocks (often represented by the S&P 500) and 40% U.S. fixed income (commonly represented by the Barclays U.S. Aggregate Bond Index or 5-year/10-year Treasuries), has long been a cornerstone of traditional investment strategy. This allocation has provided a balanced approach to growth and stability, blending the potential returns of equities with the steady income and lower volatility of bonds. However, recent market dynamics, especially the turbulent year of 2022, have put this strategy under pressure and raised questions about its continued viability.

Despite these challenges, a deeper analysis of historical data reveals that the 60/40 portfolio remains a robust option for long-term investors or intelligent investors. As we examine the historical performance of this allocation, it becomes clear that the win rate—defined as the probability of achieving positive returns—improves significantly over time.

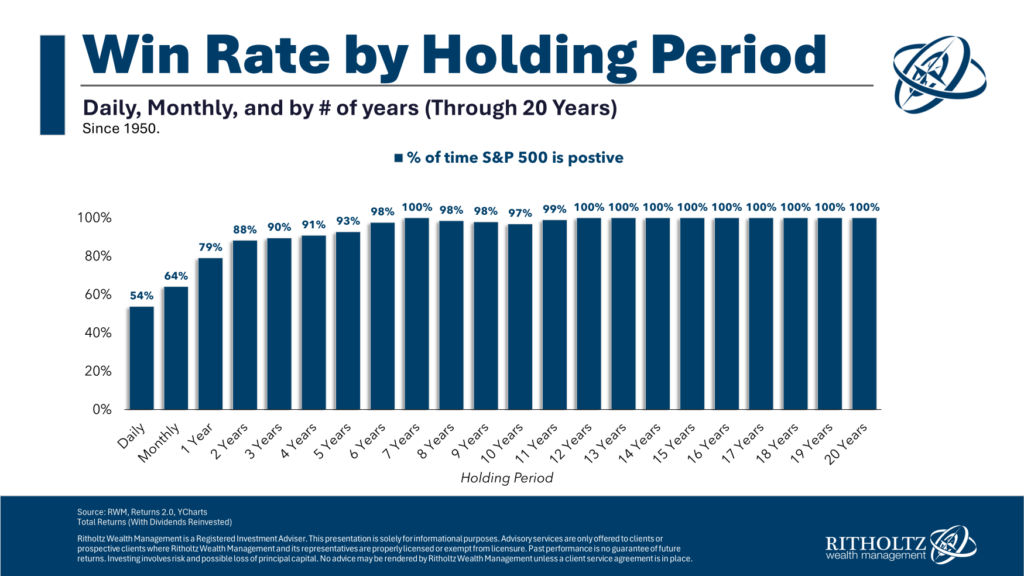

First a look at just equities- The S&P 500

As you can see from above, if you held the S&P 500 for at least 12 years, you would have a 100% win rate. But most portfolios don’t consist only of the S&P 500, so let’s dig a bit deeper and add another asset class—fixed income.

The Historical Performance of the 60/40 Portfolio

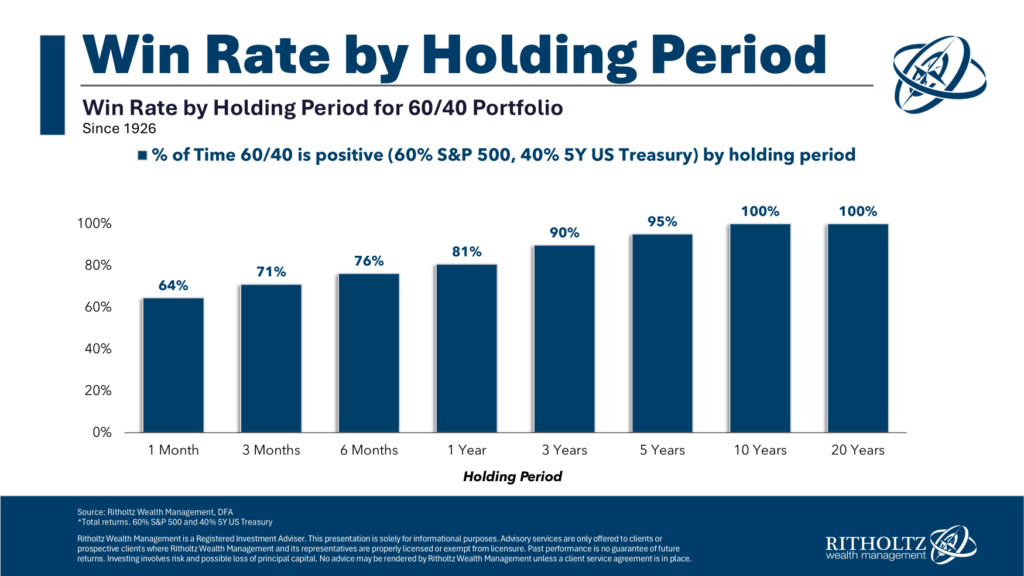

One of the key strengths of the 60/40 portfolio lies in its ability to deliver consistent returns over various time horizons. By analyzing data dating back to 1926, we can observe the resilience of this allocation across different market environments. In the examples below, the 40% allocation of fixed income is using 5 year US Treasuries as a proxy.

Monthly Returns: On a month-to-month basis, the 60/40 portfolio exhibits similar win rates to the stock market (S&P 500), albeit with slightly lower volatility. This is due to the stabilizing influence of bonds, which tend to perform well during periods of economic uncertainty.

1-Year Returns: Over a one-year period, the win rates for the 60/40 portfolio slightly outperform those of a pure equity portfolio. The inclusion of fixed income provides a cushion against market downturns, resulting in more consistent positive returns.

3-Year and 5-Year Returns: As the investment horizon extends to three and five years, the win rates for the 60/40 portfolio continue to improve. The diversification benefits of holding both stocks and bonds become more apparent, reducing the likelihood of experiencing negative returns.

10-Year Returns: Perhaps most impressively, the 60/40 portfolio has never delivered a negative 10-year return in its nearly 100-year history. This track record underscores the power of diversification and long-term investing. Even during periods of significant market stress, the combination of equities and fixed income has provided a reliable path to wealth preservation and growth.

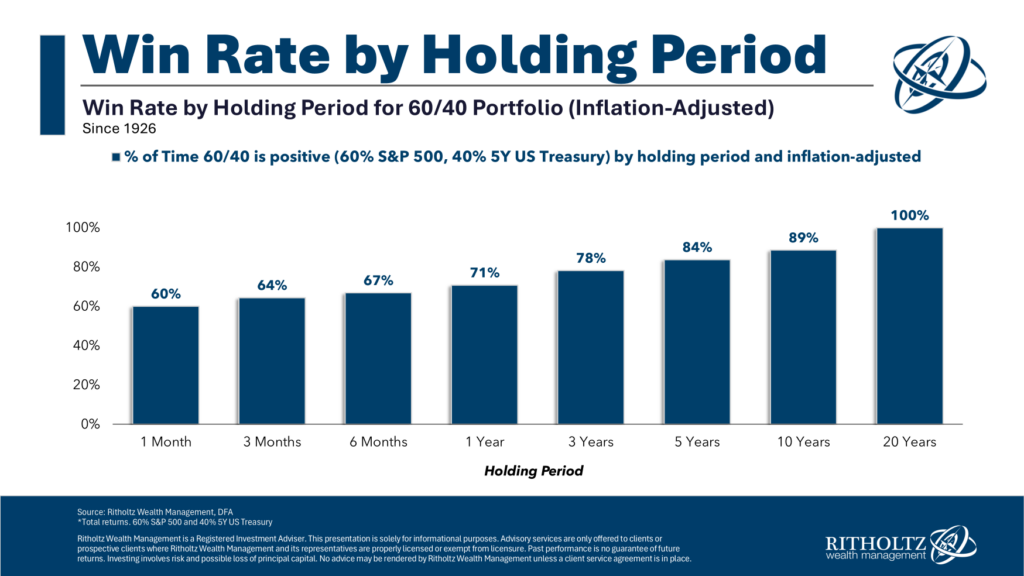

Inflation-Adjusted Returns: A Closer Look at Real Returns

While the nominal (not factoring inflation) returns of the 60/40 portfolio are impressive, it’s essential to consider the impact of inflation on purchasing power. When we adjust the historical data for inflation, the win rates do decrease slightly, but the overall trend remains positive. Even in inflation-adjusted terms, the 60/40 portfolio has delivered strong long-term returns, reinforcing its status as a dependable strategy for preserving wealth.

The Importance of Time Horizon: The data is clear—the longer your investment horizon, the higher your chances of success with a 60/40 portfolio. While short-term fluctuations are inevitable, patient investors who stay the course are rewarded with positive outcomes more often than not.

Preparing for Market Volatility

We’ve spent considerable time preparing our clients and their portfolios for periods of market volatility. By stress-testing portfolios, we provide clients with a glimpse of what their investments might look like during turbulent times. The key question now is whether to react in fear or to stick to the sound decisions that have been made.

Over the long term, equities serve as a hedge against inflation. A company’s earnings and revenues typically rise with inflation, contributing to higher stock prices. Since 1970, the MSCI USA has averaged an annualized return of 7.6%, outpacing the annualized inflation rate of around 4%. This is a testament to the power of long-term investing.

The 60/40 Portfolio as a Starting Point in Portfolio Construction

While the 60/40 portfolio has a long history of success, it is just a starting point in portfolio construction. The financial markets have evolved, and so have the strategies for building robust and diversified portfolios. There are strong arguments for enhancing the 60/40 allocation by adding other elements, such as:

- Global Diversification: Expanding the equity and bond allocation to include international and emerging markets can capture growth opportunities across the globe and provide additional risk diversification.

- Alternatives: Incorporating non-traditional assets such as managed futures, convertible bonds, and arbitrage strategies can add further diversification and reduce correlation with traditional stock and bond markets.

Private Equity and Infrastructure Funds: These investments offer access to opportunities that are often unavailable in public markets, potentially enhancing returns and providing an additional layer of diversification.

The Foundation of a Sound Investment Strategy

Before diving into portfolio construction, it’s crucial to understand your goals. Whether your objective is wealth accumulation, capital preservation, income generation, or a combination of these, your goals should guide your investment strategy. Once your goals are clear, the next step is to translate them into a well-thought-out plan. This plan then serves as the blueprint for building a diversified portfolio tailored to your unique needs.

However, even the most carefully crafted portfolio can be derailed by emotional decision-making. Headlines, market noise, and short-term volatility often tempt investors to make impulsive changes that can jeopardize long-term success. This is where Intelligent Investing comes in. We guide our clients in navigating the path to financial independence by consistently doing the right thing and avoiding the ledges of fear and greed.

Helping You Stay the Course

At Intelligent Investing, we believe that staying disciplined is key to achieving long-term success. Our approach is to help clients remain focused on their goals, avoid knee-jerk reactions to market events, and make informed decisions based on data and sound principles. By partnering with us, you gain access to expert guidance, a customized investment strategy, and the peace of mind that comes from knowing your portfolio is aligned with your goals.

We’d love to offer you a complimentary coffee or call to learn more about your financial situation and help you develop a written plan for you and your family. Visit investedwithyou.com and click on the “Get Started” button to begin your journey to becoming the next intelligent investor.