Reading Time: 3 minutes

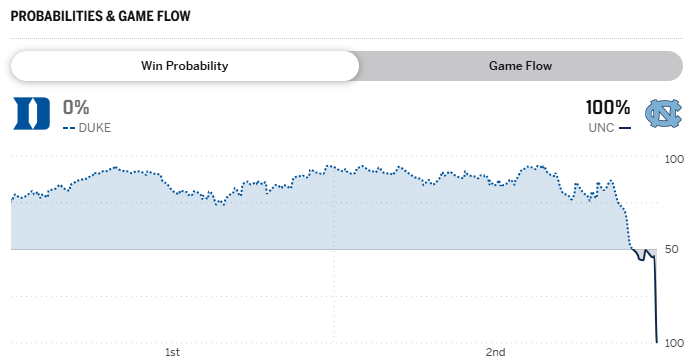

The legendary rivalry of the recent UNC vs. Duke buzzer-beater is a masterclass in why you play until the very last second. For nearly 40 minutes, the Tar Heels were down. They trailed for the entire first half and 19 minutes and 59 seconds of the second.

With 7 minutes to go, the models gave Duke an approximate 95% chance of victory. But the only scoreboard that mattered was the one that read “UNC 71 – Duke 68” after Tarheel Seth Trimble made a clutch 3-pointer in the corner with 0.4 seconds to win the game.

Sports fanatics call that a legendary comeback.

In your financial life, it’s a warning: Halftime leads don’t matter if you make a split-second mistake at the finish line of your retirement.

The Subtle Rivalry: You vs. the “Common Sense” Narrative

You hear it every day on the radio and see it on TV—the loud pitches for “guaranteed” products that claim to be the only “common sense” way to protect your retirement. It’s easy for a family member to fall into this trap, especially when a slick insurance salesman makes a complicated annuity contract sound like a “sure thing.”

But as the CFA Institute often points out, what sounds like “common sense” in a 30-second commercial can be a strategic disaster for high-net-worth families:

- The Tax Penalty on Your Legacy: This is the most dangerous “blind spot.” Unlike traditional investments that benefit from lower capital gains rates and a “stepped-up basis” at death, annuity gains are often taxed at higher ordinary income rates. Passing an annuity to the next generation can inadvertently hand the government a massive portion of your family’s wealth.

- The Performance Ceiling: Many of these products utilize “caps” that act like a coach benching his star players the moment they start scoring. If the market grows 20%, but your return is capped at 5%, you aren’t winning—you’re losing the compounding growth required to stay ahead of inflation.

- The Liquidity Trap: A championship team needs to be nimble. Most of these “guaranteed” contracts are illiquid, locking your capital away behind hefty surrender charges. If your family needs to pivot, your money is stuck on the bench.

Don’t Turnover the Final Possession

At Intelligent Investing, we see these “common sense” mistakes frequently. One split-second decision with a salesman can ruin a whole generation’s wealth.

That is why we offer a specialized “Annuity Rescue Program.” We help families analyze these complex contracts to see if they are truly serving their long-term goals or simply serving the insurance company.

If you have $1M–$10M in investable assets and want to ensure your wealth—and your family values—are passed carefully to the next generation, don’t settle for a catchy slogan.

Reach out to our team today for a complimentary call and no pressure second opinion.

Let’s use our proprietary Intelligrations® framework to build a playbook that ensures you’re leading when the final buzzer sounds.

Get Started!